The Reserve Bank (RBA) has lifted the cash rate to 4.35%, prompting Treasurer Jim Chalmers into saying, ‘(it) won’t make it any easier for millions of Australians with a mortgage.’ It is the third rate hike in 2026 and the RBA Governor Michele Bullock warns more interest rate rises could come ‘to ensure we get on top of inflation’, while admitting, ‘These interest rate rises are not going to do anything for inflation in the next six months.’

Meanwhile, both business and consumer confidence has collapsed to recessionary levels. The NAB Business Confidence Index plunged to -29 in March 2026 after the first rate shock – the second-largest monthly drop on record and the weakest since April 2020. The Roy Morgan Business Confidence for April shows the index crashing 14.2 points to a record low of only 76.5.

Following last two rate hikes, the Westpac–Melbourne Institute Consumer Sentiment Index fell heavily in April, declining 12.5% to 80.1 from 91.6 in March. The latest ANZ-Roy Morgan Consumer Confidence Rating fell to 67.2 – nearly 30 points below the neutral level of 100 – in early May before the RBA meeting. This is the seventh-lowest Consumer Confidence reading of all-time.

Unsurprisingly, a day before the RBA Board meeting, Gary Morgan, Michele Levine and Julian McCrann argued, ‘the Reserve Bank should not raise interest rates tomorrow with Business Confidence and Consumer Confidence at, or near, record lows and real unemployment near a record high.’ They also warned, ‘it would be a mistake for the RBA to increase interest rates tomorrow and ignore the key economic indicators that show the Australian economy is already in a weakened state, and perhaps already in a recession. If the RBA does raise interest rates tomorrow, it would most likely plunge Australia into a ‘recession we don’t have to have’ – if we aren’t already in one.’

It seems the RBA has not learnt any lesson from the past mistakes of central banks; nor has it learned from Australia’s own experience in dealing with inflation without forcing a recession.

Inflation phobia and policy over-reaction

Central Banks around the world suffer from inflation phobia, and the RBA is not an exception. They fear inflation expectations becoming unhinged fuelling ‘wage-price spirals’, and thus a run-away or accelerating inflationary situation which is harmful for the economy in the long-run. However, quite often this inflation phobia results in excessive monetary tightening.

The former US Federal Reserve Chair, Ben Bernanke and his co-researchers found that the output declines or recession in the 1970s did not result from the oil-price shocks ‘per se, but from the resulting tightening of monetary policy.’ Bob Barsky (National Bureau of Economic Research) and Lutz Kilian (European Central Bank) made ‘the case that the oil price increases were not nearly as essential a part of the causal mechanism generating the stagflation of the 1970s as is often thought.’ Ed Nelson (US Federal Reserve Board) blamed central banks’ ‘faulty doctrine’ for the 1970s stagflation.

So, it was not inflation that caused output to decline, but rather, inappropriate and draconian efforts to curb inflation that inevitably repressed growth, and produced the world’s first stagflation. This may happen again as central bankers over-react and tighten the financial conditions to kill the current inflation, which the International Monetary Fund (IMF) attributes to ‘textbook supply shock.‘

It’s the group-thinking, stupid

The problem is the central bankers’ dogmatic group-thinking despite contrary empirical evidence. For example, the fear of unhinged inflation expectations and wage-price spirals do not have any empirical basis. Research within the RBA has found that ‘the overall risk [of wage-price spirals] in most advanced economies is … quite low, and certainly lower than in the 1970s’, primarily due to the declines in labour bargaining power. Similarly, The IMF research has found ‘a limited risk of a wage-price spiral and regime shift in inflation expectations in response to supply shocks. For the past several decades … [there was] no evidence of oil price shocks leading to a sustained wage-price spiral that would have pushed up the inflation rate for a sustained period (nor permanently).’

Yet, the central bankers, including the IMF, favour monetary tightening arguing the risk of ‘unhinged’ or ‘unanchored’ inflation expectations and wage-price spirals. Ironically the IMF also warns that such tightening is likely to be ‘more costly’ in terms of lost output as the aggregated supply curve has become flatter. The RBA Governor also acknowledges that ‘monetary policy trade-offs have become significantly harder.’

Interest rate over-dose

The RBA Governor says unfortunately the interest rate is the only medicine that the RBA has to cure inflation even though it knows interest rate hikes cannot fix supply bottlenecks. Instead, rate hikes can exacerbate supply problems. Interest rate hikes will also have collateral damages on government finance, besides causing job losses and economic hardship for struggling families.

Interest rate is a blunt tool; it does not distinguish between households and businesses. Higher interest rates may encourage households to save, but dampen business spending. Thus, economy-wide demand may shrink discouraging investment in new technology, plants and equipment as well as skill-upgrading, adversely affecting long-term productive capacity. The Economist has observed, ‘Drooping demand crimped incentives to invest and innovate’ and attributed declining UK productivity growth to cutbacks in innovation spending due to ‘austerity policies’ and ‘severe reduction in credit’ among other factors.

Interest rate also does not distinguish between efficient and inefficient business activities. Raising interest rates too often and by too much can disrupt productive and efficient businesses and investments. Thus, even efficient and productive enterprises may face liquidity or cash-flow problems while inefficient and less productive businesses cease to operate. This can, in turn, cause strains for the banking sector as the IMF’s Global Financial Stability Report 2023 warned.

Higher interest rates will strengthen Australian dollar which may have moderating impact on imported inflation. But a stronger dollar will adversely impact price-sensitive manufacturing exports. Our tourism sector is especially vulnerable to a stronger dollar.

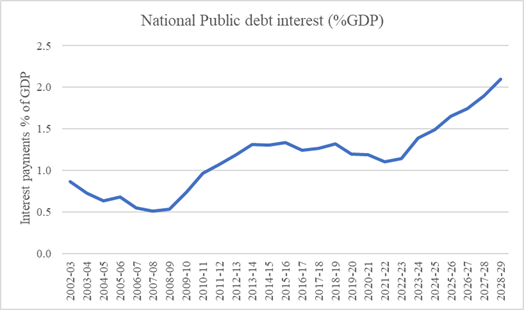

Higher interest rates will raise the debt burden for governments, business and households. Debt burdens have been on the rise since the 2008-2009 global financial crises. The IMF has already warned that a prolonged war in the Middle East could further raise Australia’s debt, which is expected to hit A$1 trillion within months. Even if the government does not borrow, its debt burden will grow due to interest rate rises. The Parliamentary Budget Office’s December 2025 National Fiscal Outlook, estimated that national public debt interest payments would increase markedly from 1.7% of GDP in 2025‑26 to 2.1% of GDP in 2028‑29. This year’s three consecutive interest rate over-dose will only worsen the outlook.

Source: PBO, 2025-26 National Fiscal Outlook, 4 December 2025

According to the Australian Bureau of Statistics (ABS), Australian household debt has reached record highs, with total liabilities climbing to A$3.33 trillion by June 2025. Australia’s household debt (approximately 112% of GDP) is now second highest globally. The third rate hike in a row ‘has delivered a blow not only to mortgaged homeowners, but also to those hoping to break into the property market.‘ This will certainly worsen inter-generational inequality which has already been accelerating due to higher interest rates.

In February, Business NSW warned, a 25bp interest rate hike could cost small businesses A$1 billion over five years, tightening cashflow, risking jobs and investment. The latest RBA rate hike will cause more pain for businesses.

Revisiting the inflation target

The central bankers’ group-thinking bias insists on an inflation target of 2% – a figure ‘plucked out of the air‘ that became ‘global economic gospel.‘ Don Brash, the acclaimed former Governor of the Reserve Bank of New Zealand, who was the first central bank governor to adopt a 2% inflation target admitted that it was based on a chance remark by then New Zealand Finance Minister Roger Douglas ‘during the course of a television interview.’ It became ‘the mantra, repeated endlessly’ as Brash and his colleagues ‘devoted a huge amount of effort’ to preaching his new gospel ‘to everybody who would listen – and some who were reluctant to listen.’

Olivier Blanchard, the IMF’s former Chief Economist, questioned the wisdom behind the 2% inflation target and argued for a higher, e.g., 4% target following the 2008-2009 global financial crisis. Research within the IMF also advocated for the case for a long-run inflation target of 4%. Such a moderately higher inflation should widen policy space.

Joe Gagnon and Chris Collins of the conservative think-tank, Peterson Institute for International Economics, have argued that ‘the case for raising the inflation target is stronger’ than it is usually thought. Their research shows that ‘the benefits [of a higher inflation target] clearly exceed the costs.’ Daniel Leigh has found that ‘a higher inflation target could have halved the output loss of Japan during its ‘Lost Decade’.’

Thus, one should not be surprised when The Financial Times says, ‘It is time to revisit the 2% inflation target.’

After reviewing the RBA’s inflation targeting framework over more than two decades, Warwick McKibbin and Augustus Panton concluded, ‘the nature of future shocks suggests that some form of nominal income targeting is worth considering as an evolutionary change in Australia’s framework for monetary policy.’

Rethinking inflation

Almost all central bankers see inflation as an outcome of excess demand, caused by either a rightward shift of the aggregate demand curve or a leftward shift of the aggregate supply curve. A common view is that excess demand would work its way from a tight labour market, to higher wages, to higher prices. Thus, their policy focused on containing demand by raising interest rates regardless of the sources of inflation.

Considering inflation is the result of a distributional conflict or disagreement, Guido Lorenzoni and Iv´an Werning of MIT analysed impacts of supply shocks arising from ‘non-labour’ inputs, such as energy, under different relative bargaining power of labour and firms and where the non-labour input price is perfectly flexible, and goods prices are more flexible than wages.

They have found that the optimal policy response to a supply shock coming from the scarce non-labour input is to ‘run the economy hot’ with a positive output gap to attain high inflation. It may be more efficient to reach the adjustment with the help of higher price inflation and moderate wage deflation, rather than though lower price inflation and deeper wage deflation through higher unemployment.

They have also explored cases where it is optimal to have both wage and price inflation. They have noted, ‘A positive output gap helps shift the adjustment in the direction of price inflation, so is socially beneficial.’

David Ratner and Jae Sim, both on the Board of Governors of the Federal System of the US, have analysed the trade-off of anti-inflationary measures considering inflation as an outcome of distributional conflict. They have developed, the ‘Kaleckian Phillips curve’, its slope being determined by the bargaining power of trade unions.

According to them, the declines in the relative bargaining power of labour since the early 1980s following the labour market deregulation ‘killed’ the conventional Phillips curve while the slope of the Kaleckian Phillips curve became flatter, thus, making restrictive anti-inflationary measures more costly in terms of unemployment. They have presented robust econometric evidence – both time series and cross-sectional – in support of their theoretical analysis.

Interestingly, their finding corroborates with the IMF’s observation that the aggregate supply curve has become flatter making restrictive anti-inflationary measures more costly in terms of lost output. Unfortunately, the central bankers’ anti-inflation group bias dismisses the higher unemployment or growth declines due to restrictive policies as ‘short-term pains for long-term gains.’

However, IMF research has revealed permanent scars of recessions, including those arising from external shocks and small domestic macroeconomic policy mistakes. They all ‘lead to permanent losses in output and welfare’, while The Lancet has reported ‘substantial effects on suicide rates.’ In The Body Economic: Why Austerity Kills, David Stuckler and Sanjay Basu have investigated the human cost of austerity policies during economic crises to emphasise that health indicators can significantly deteriorate.

Optimal policy response

The government has been trying to ease fuel-price impacts by fiscal measures such as reducing fuel excise duty and changes to fuel tax credit rates. The Federal Government, in partnership with state and territory governments, has also adopted national fuel security plan with the aim of ensuring affordable supply of fuel.

Although 83% of Australians approve of the Government’s response to the fuel crisis, the mainstream commentators, including the IMF, oppose such measures. They argue that these measures may have significant fiscal costs if the crisis lingers on, and hence would put extra-burden on the RBA focused on controlling inflation.

Precisely for that reason the optimal policy response should include measures to raise tax revenues. As the Treasurer is preparing the forthcoming May budget, he should consider enhancing tax progressivity. In particular, an excess profit tax should be imposed on the beneficiaries of higher interest rates and fuel prices, such as banks and fuel companies to fund cost of living support measures. The Guardian has recently reported, ‘As regular Australians struggle, gas companies are making massive profits and paying minimal tax.’

Former Treasury Secretary Dr. Ken Henry has argued that a 100% tax on windfall profits from gas is ‘socially optimal’, while Grattan Institute’s Tony Wood argued ‘A windfall profit tax may be the least-worst solution to the gas crisis.’ Research with the US data reveals that an excess profit tax reduces existing racial and ethnic inequalities and inequalities between groups with different educational attainments. It can also accelerate renewable energy transition when increasing geopolitical tensions and climate impacts threaten continued volatility in fossil fuel and gas markets.

Recently the IMF has suggested ‘taxing harmful habits.‘ Excise taxes on unhealthy products like alcohol, tobacco, and sugar are an attractive way to both mobilise much-needed domestic tax revenue and encourage healthier behaviour. The IMF observes ‘sin’ or ‘behavioral’ taxes have existed for millennia, but fresh challenges have arisen in recent years as a plethora of new products have entered the market, from e-cigarettes to low-alcohol beer.’

Addressing supply bottlenecks can involve tax incentives and differentiated credit policies. However, discredited supply-side solutions – e.g. more labour market deregulation, or further tax cuts for the rich and for foreign investors – must be exposed and discarded. Differentiated credit and tax incentive policies should optimise liquidity and credit allocation, to support key sectors, while avoiding bubbles and overheating in sectors such as real estate or industries with overcapacity. In this regard, much can be learnt from the People’s Bank of China’s ‘structural monetary policy.‘

However, this would require macroeconomic policy coordination with sectoral strategies. Paul McCullay and Zoltan Pozsar concluded, ‘fiscal-monetary cooperation … can help solve the problem that each authority faces on its own … in the cooperation framework the central bank overtly subjects itself to become a partner of the fiscal authority in stimulating economic growth.’

According to Willem Buiter, fiscal-monetary policy coordination can create fiscal space, but it is up to the government ‘to make appropriate use of this fiscal space.’ This is the key point – monetary policies should be designed to finance needed productive public investments – e.g., in infrastructure, renewable energy, education, healthcare.

Finally, we need to recognise that inflation is a result of distributional conflict. The fear of so-called second-round effect arises precisely from distributional conflict between business and labour. Certainly, workers bargaining power has waned, but cost of living pressure has significant political implications.

The hall-mark of the Hawke-Keating Government was the Prices and Incomes Accord, signed in 1983 with the Australian Council of Trade Unions (ACTU) aimed at curbing high inflation and unemployment. The agreement underpinned the economic success and social progress of the Hawke-Keating era. It showed what is possible when unions, government and business truly collaborate.

Anis Chowdhury is an associate of the Centre for Future Work. He is a highly regarded development and heterodox macroeconomist who has published close to 100 research articles, more than two dozen books, and has penned numerous opinion pieces on contemporary economic, social and geo-political issues.