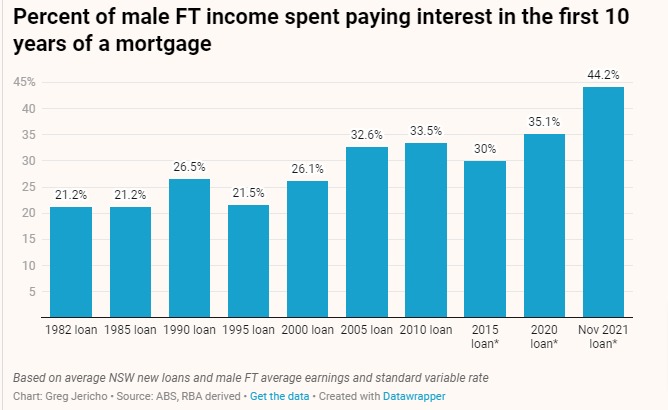

For most of the past decade the talk about housing affordability has focussed on house prices. As fiscal policy director, Greg Jericho notes in his Guardian Australia column, falling interest rates since November 2010 have made paying off a mortgage less onerous than it otherwise would have given the soaring house prices.

But that is about to change.

The signal that interest rates are going to rise by possibly 2.5% points over the next 18 months means that for new mortgage holders the cost of repaying a mortgage is going to be harder than ever before – harder even than when interest rates hit 17% in 1990.

It is a hit that will only exacerbate standard of living problems as wages will struggle to keep up with the rising cost of of holding a mortgage – especially given the belief that wage rises need to be contained below inflation rises continues in economic debate.

You might also like

Chalmers is right, the RBA has smashed the economy

In recent weeks the Treasurer Jim Chalmers has been criticised by the opposition and some conservative economists for pointing out that the 13 interest rate increases have slowed Australia’s economy. But the data shows he is right.

Analysis: Will 2025 be a good or bad year for women workers in Australia?

In 2024 we saw some welcome developments for working women, led by government reforms. Benefits from these changes will continue in 2025. However, this year, technological, social and political changes may challenge working women’s economic security and threaten progress towards gender equality at work Here’s our list of five areas we think will impact on

Would you like a recession with that? New Zealand shows the danger of high interest rates

New Zealand’s central bank raised interest rates more than Australia and went into a recession – twice.