The latest raise in the cash rate has meant interest rates have increased by more in 4 months than they have anytime since 1994.

This is expected to have a dramatic impact on the economy with the Governor of the Reserve Bank announcing that the RBA expects GDP growth in 2023 and 2024 to be just 1.75%.

Labour market and fiscal policy director, Greg Jericho, in his Guardian Australia column, notes that this would be the the first time since the 1990 recession that there have been 2 consecutive years of growth below 2%.

The steep rise in rates, and the prospect of more to come suggests that the Reserve Bank’s efforts to curb inflation are likely to come at a high cost for workers.

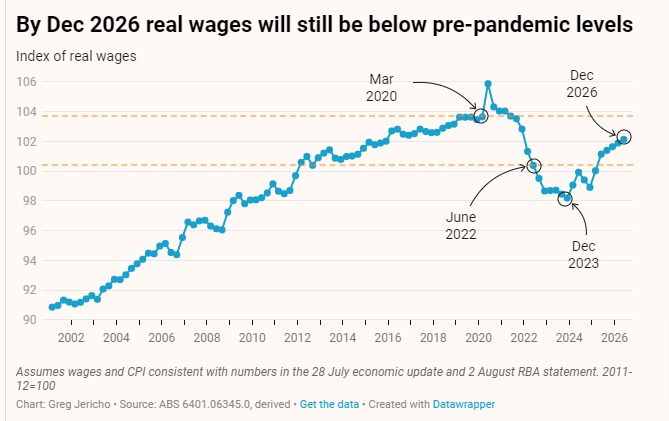

The past year has seen the biggest fall in real wages since the introduction of the GST and current estimates from the Treasury and the Reserve Bank suggest further falls to come until the end of next year. By that point real wages would be more than 5% below pre-pandemic levels – a truly disastrous result in what is supposedly a recovery period.

You might also like

Chalmers is right, the RBA has smashed the economy

In recent weeks the Treasurer Jim Chalmers has been criticised by the opposition and some conservative economists for pointing out that the 13 interest rate increases have slowed Australia’s economy. But the data shows he is right.

Analysis: Will 2025 be a good or bad year for women workers in Australia?

In 2024 we saw some welcome developments for working women, led by government reforms. Benefits from these changes will continue in 2025. However, this year, technological, social and political changes may challenge working women’s economic security and threaten progress towards gender equality at work Here’s our list of five areas we think will impact on

Would you like a recession with that? New Zealand shows the danger of high interest rates

New Zealand’s central bank raised interest rates more than Australia and went into a recession – twice.