Wages Crisis Has Obvious Solutions

Mainstream economists and conservative political leaders profess “surprise” at the historically slow pace of wage growth in Australia’s labour market. They claim that wages will start growing faster soon, in response to the normal “laws of supply and demand.” This view ignores the importance of institutional and regulatory factors in determining wages and income distribution. In fact, given the systematic efforts in recent decades to weaken wage-setting institutions (including minimum wages, the awards system, and collective bargaining), it is no surprise at all that wages have slowed to a crawl. And the solutions to the problem are equally obvious: rebuild the power of those institutions, to support workers in winning a better share of the economic pie they produce.

This recent commentary, by Centre for Future Work Director Jim Stanford, appears in the March 2018 issue of Australian Options magazine, and is reprinted with permission.

Wage Crisis Has Obvious Solutions

By Jim Stanford

When the head of the central bank declares wages are too low, and urges workers to demand more money, you know you have a problem.

After all, central bankers are traditionally the “party poopers” of the economy: they are the ones who march in and take away the punch bowl, as soon as the party gets rolling. Yet here was Governor Philip Lowe, Governor of the Reserve Bank of Australia, urging party-goers to turn up the volume. It’s like he was pouring bottles of straight tequila into the punchbowl, instead of taking it away – desperately trying to turn a boring flop into a wild shindig.

Mr. Lowe made his surprising call at a conference last year on Australia’s economic outlook at Australian National University. He said weak wage growth was holding back national purchasing power and economic growth, and contributing to too-low inflation (which has languished below his bank’s official 2.5 percent target for several years running).

But while his acknowledgement of the consequences of wage stagnation was refreshing, his diagnosis of the causes was incomplete and unconvincing. In fact, Governor Lowe almost seemed to blame the victims of wage stagnation – namely, Australia’s workers – for the problem. They were unduly worried about losing their jobs to robots or imports, he suggested; they should feel more “confident” in asking for higher wages. He has clearly not experienced the reality of Australia’s dog-eat-dog labour market in recent years, or felt the desperation that drives workers, especially young workers, to accept any job on offer.

(Incidentally, the RBA’s own enterprise agreement signed last year will raise base wages by just 2 percent per year over the next 3 years … below the bank’s own inflation target!)

While mainstream economists and policy-makers belatedly recognise the economic and social damage resulting from weak wages (even Treasurer Scott Morrison frets about the negative effect of slow wage growth on his budget balance), they’ve been distinctly reticent to connect the dots about the causes of the problem – and its obvious solutions. Lowe, Morrison, and their colleagues pretend wages will pick up automatically as the economy grows and the labour market tightens. But with official unemployment only a tick above 5 percent (still the RBA /Treasury estimate of “full employment,” according to their discredited but still operational NAIRU model), yet wages still decelerating, this faith in a market solution is increasingly far-fetched.

Measuring the Slowdown

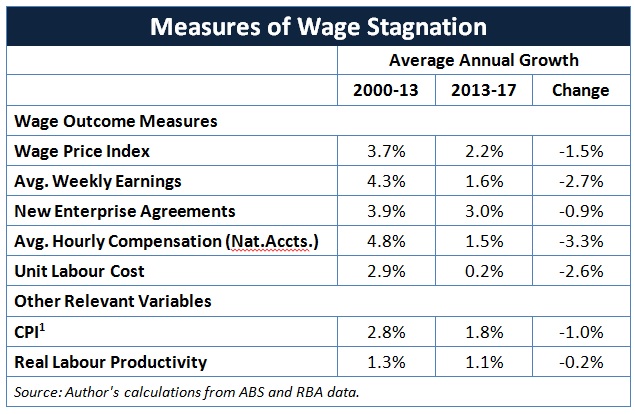

The stagnation of Australian wages is visible by many indicators. The most common “headline” source is the ABS’s quarterly Wage Price Index, which reports an index of wages calculated from a representative sample of jobs (the methodology is similar to the Consumer Price Index). The WPI therefore measures changes in average hourly compensation holding constant the bundle of jobs which make up the overall labour market.

However, one important factor in weak wages has been the changing composition of work. In particular, the growth of part-time, casual, and irregular jobs has undermined the overall level (and stability) of labour incomes. These changes are not captured in the WPI. Similarly, changes in average hours worked per week (due to growing part-time work) are also excluded from the WPI. So the WPI data understates the true extent of the wage slowdown.

Other ways of measuring the wage slowdown show an even bigger drop-off in wage growth. These include average weekly earnings, the pay increases specified in enterprise agreements, and estimates of average labour compensation generated through GDP statistics. Trends in all these indicators are summarised in the accompanying table. Whatever measure is chosen, it is clear that there has been a dramatic slowdown in wage growth – especially visible since 2013.

Annual wage growth fluctuated around 4 to 5 percent during the first decade of the century. Wage growth fell sharply but temporarily during the GFC – but then quickly regained pre-crisis norms from 2011 through 2013. After 2013, however, wage growth has decelerated dramatically: to 2 percent or even lower. In fact, by the broadest measure of labour compensation (wages, salaries, and superannuation contributions paid per hour of work), there has been virtually no nominal wage growth in the past year. Consumer prices, meanwhile, continue to grow at around 2 percent per year (and even faster, if escalating housing prices are taken into account). Real earnings, therefore, are flat or falling.

What is “Normal” Wage Growth?

Any shortfall in wage growth below the pace of consumer price increases (corresponding to a decline in the real purchasing power of workers’ incomes) is a clear sign of labour market dysfunction. But even flat real wages (ie. nominal wages that just keep pace with inflation) are problematic. After all, wages are supposed to reflect ongoing growth in real labour productivity (or at least that’s what the economics textbooks tell us). So wages should actually consistently grow faster than consumer price inflation, to fairly reflect the enhanced real output of each hour of labour.

Therefore, a “normal” benchmark for wage growth might be the sum of long-run consumer price inflation (the RBA’s 2.5 percent target) plus average productivity growth (running around 1.5 percent per year over the past three decades). That suggests a “normal” benchmark for annual nominal wage growth should be 4 percent per year. Australian wage growth in the pre-GFC period generally fit that definition of “normal.” But since 2013 wages shifted to a significantly lower trajectory.

Joining the Dots

Contrary to the assumptions of free-market economics, there is no guarantee that wages will automatically grow in line with labour productivity, as a result of automatic market mechanisms. Power is always a key factor in income distribution. And labour markets never “clear,” so that labour supply (the number of workers) equals labour demand (the number of jobs). In fact, inflation-targeting policy deliberately aims to maintain a certain level of unemployment (5 percent is the target in Australia) to suppress wage demands and protect profits.

The systematic and structural disempowerment of workers and their unions over the neoliberal era is therefore the most relevant factor in the deceleration of wage growth, and the erosion of labour’s share of total GDP. Some obvious indicators of that dramatic shift in economic and political power include:

- A steady erosion in the real “bite” of minimum wages, which have fallen from 60 percent of median wages in 1990 to around 45 percent today.

- The collapse of trade union membership in the face of legal restrictions, harassment, and full-protection for “free riders.” Today just 9 percent of private sector workers, and less than 5 percent of young workers, are union members.

- A corresponding collapse in collective industrial action. Adjusted for the size of the workforce, the frequency of strikes and other industrial disputes has declined by 97 percent from the 1970s to the present decade.

- The relegation of industry awards to a baseline “safety net,” instead of a system for supporting ongoing progress in wages and working conditions.

- The generally pro-business shifts in economic policy, including tax cuts, deregulation, privatisation, and globalisation, which have also shifted economic power in favour of employers and hence indirectly suppressed wage growth.

To begin to rebuild wage growth, restore labour’s share of GDP, and achieve greater equality in labour incomes will require a comprehensive, multidimensional effort to restore the power of all these wage-supporting institutions. The ACTU is tackling this challenge with gusto, with its ambitious “Change the Rules” campaign. The goal is to propose a consistent, holistic vision for repairing the institutions that support workers and their wages – and then building a strong grass roots campaign to push politicians of all stripes to adopt that vision.

On the other hand, if we follow the advice of Scott Morrison and Philip Lowe, and simply wait for supply and demand forces to rescue wages from their current doldrums, we are going to be waiting a very long time.

You might also like

The 9 to 5 is back! Time to put the phone on silent

If you’ve ever flicked off an email before bed, texted your boss out of hours, or received an ‘urgent’ work call after clocking off, you’ll be glad to hear some respite is just around the corner. A new right to disconnect from work, for employees in businesses with 15 or more staff, comes into force

Analysis: Will 2025 be a good or bad year for women workers in Australia?

In 2024 we saw some welcome developments for working women, led by government reforms. Benefits from these changes will continue in 2025. However, this year, technological, social and political changes may challenge working women’s economic security and threaten progress towards gender equality at work Here’s our list of five areas we think will impact on

The continuing irrelevance of minimum wages to future inflation

Minimum and award wages should grow by 5 to 9 per cent this year